New income tax return forms with fresh requirements

TG Team taxguru.in/income-tax/income-tax-return-forms-fresh-requirements.html

taxguru.in/income-tax/income-tax-return-forms-fresh-requirements.html

Every year, the CBDT notifies the new income

tax return forms and for the assessment year 2018-19 also CBDT has

released the new income tax return forms. These forms will be applicable

for the income tax return of 01-04-2017 to 31-03-2018 period. With the

help of this write up we will be able to understand the new information

required in these forms so that before filing the returns the assessee

shall be ready with the desired information.

It is apparent with the changes that the new

ITR Forms shifts the onus on the taxpayers to prove their claim for

deductions, expenses or exemptions. These ITR forms seek more

information from trusts, taxpayers who opted for presumptive taxation

scheme, investors in shares of unlisted companies, so on and so forth.

Let us discuss the changes in detail:

1. Calculation of salary income in detail:

(Changes relevant for ITR-1,2,3,4)

The new ITR form (1, 2, 3 and 4) requires

detailed calculation of income from salary, which was restricted to

single figure till last year. This will increase the transparency

between the assessee and department. The assessee may get these

information from Form 16 (Part B) issued by the employer.

2. Non-Residents to file ITR Form 2 or 3:

2. Non-Residents to file ITR Form 2 or 3:

(Changes relevant for ITR 1,2,3)

The Form ITR-1 (SAHAJ) shall be filed by the Individual being resident

other than not ordinarily residents having income from salary, one

house property and other sources (Interest, etc.) with the Total income

of Rs. 50 Lakhs.

Therefore, the Non-resident shall not be able to file the ITR-1 anymore. A non-resident will have to choose either form ITR-2 or ITR-3 to file the return of income for the Assessment Year 2018-19.

3. File ITR 3 by a Partner of firm:

(Changes relevant for ITR 3)

For the Assessment Year 2018-19, an individual

or an HUF, who is a partner in a firm, shall be required to file his

ITR in Form ITR 3 only. Last year the partners had an option to file

return in ITR 2.

4. Information required in relation to Sale of un-quoted shares:

[Changes relevant for ITR 2, 3, 5, 6, 7]

As per the requirements of section 50CA of

Income tax act, 1961, the new form requires following information as per

the screen shot. In case capital gain arising on transfer of unquoted

shares, it would now be mandatory for the investors to obtain the valuation report as the

new ITR forms require the taxpayer to provide figures of actual sales

consideration and FMV as determined by a Merchant Banker or CA.

5. Taxability of gifts under other sources:

[Changes relevant for ITR 2, 3, 5, 6, 7]

Earlier any sum of money or any property

received for without consideration or inadequate consideration (in

excess of INR 50,000) was subject to income from other sources as per

section 56(2)(vii). Effective from AY 18-19, a new provision has been

inserted vide section 56(2)(x) to include any taxpayer within the ambit.

Therefore, from AY 18-19, any person receives

money or any property for without or inadequate consideration (in excess

of INR 50,000) shall furnish the information of the same and pay the

tax accordingly.

6. More reporting in presumptive taxation scheme

(Relevant for ITR 4)

In case a taxpayer opts for presumptive

taxation scheme under section 44AD, 44ADA or 44AE, he will have to file

the return of income in form ITR 4. The old ITR 4 sought only four

financial particulars of the business,

(a) total creditors,

(b) total debtors,

(c) total stock-in-trade and

(d) cash balance.

The new ITR 4 form seeks details of 14

financial particulars of business such as amount of secured/unsecured

loans, advances, fixed assets, capital account, etc. However, fields

other than Total creditors, total debtors, cash in hand and stock in

trade is not compulsory.

7. Aggregated turnover reported in GST returns:

(Relevant for ITR 4)

The new ITR 4 requires a taxpayer to provide

the aggregate turnover reported by him in GST Returns. This additional

information has been sought to end the wrong practice of reporting

different turnovers in erstwhile sales tax return and income-tax return.

If any difference is found in turnover reported in GST return and ITR,

presumptive taxpayers can expect a notice from the Dept. to explain the

mismatch in turnover.

8. Reporting of expenditure with registered and un-registered entities:

(Relevant for ITR 6)

The companies who are not required to get the

accounts audited under section 44AB of Income tax act, 1961 shall

furnish the following transaction (expenditure) in the ITR-6:

- Transactions in exempt goods or services

- Transactions with composite suppliers

- Transaction with registered entities and total sum paid to them

- Transaction with unregistered entities

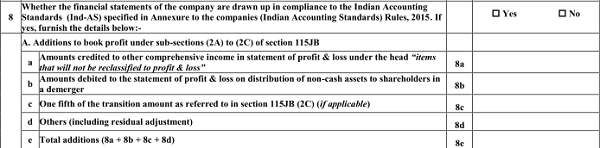

9. IndAS compliant companies to provide additional information:

(Relevant for ITR 6)

Though the IndAS is applicable on High Net

Worth companies (INR 500 Crores or more as on 31-03-14) w.e.f.

31-03-2017 but no requirement was there in the ITR form for AY 2017-18.

However, for AY 2018-19, the ITR 6 introduces a new schedule for Ind AS

Compliant companies wherein they shall be required to disclose the Ind

AS Financial Statements.

Further, to calculate the book profit

correctly, in case of Ind AS compliant companies, ITR 6 now incorporates

changes to include the adjustments of debit/credit to “Other

comprehensive income” and other items.

10. Penalty on late filing of Income tax return:

(Relevant for ITR 1 to 7)

The assessee shall be required to file the

return before the due date as may be applicable. Until last year, if a

taxpayer failed to file the ITR before end of assessment year, penalty

under Section 271F could be imposed by the Assessing Officer only after

initiating the penalty proceedings.

After omission of this penalty provision by

the Finance Act, 2017, late fees is levied under Section 234F if

taxpayer does not furnish the ITR in time. The taxpayer shall now be

required to pay late filing fees under section 234F along with interest

under section 234A, 234B and 234C before filing the ITR.

11. Rate of depreciation:

(Relevant for ITR 3, 5, 6)

As per 29th Income tax amendment rules, 2016, CBDT has restricted the rate of depreciation to maximum up to 40% for any block of assets.

Therefore, new forms has replaced the column of depreciation from 50%/60%/80%/100% to 40%.

Further, new columns has been added to include proportionate depreciation in case of demerger, amalgamation, etc.

In case the asset is not used exclusively for business purpose, a separate disclosure can be made in section 38(2).

12. Capital gains exemptions:

(Applicable for ITR 2, 3, 5 and 6)

The new ITR Forms introduce specific columns to report each capital gain exemption

separately. Details of each capital gains exemption under Sections 54,

54B, 54EC, 54EE, 54F, 54GB and 115F shall be reported in its applicable

column now.

Further, a taxpayer availing of these capital gains exemptions is required to mention the date of transfer of original capital asset which was missing in earlier ITR Forms.

13. Reporting to claim the benefit of DTAA relief:

(Relevant for ITR 2, 3, 5 and 6)

The assessee claiming DTAA relief in respect of capital gains or income from other sources are required to provide details of applicable DTAA.

The new ITR Forms seeks following additional details for current year:

14. Impact due to ICDS deviation:

(Relevant for 3, 5 & 6)

The tax payer has to report the deviation of

ICDS as profit and loss separately. Till now, the reporting was required

to net impact (negative or positive) only.

15. Particulars of individual beneficial owners:

(Relevant for ITR 6)

Particulars of natural persons who were

beneficial owners of shares holding not less than 10% of the voting

power at any time of the previous year shall be reported in the ITR-6.

16. Changes with respect to Trusts:

(Applicable for ITR 7)

- Additional information required to be disclosed in the ITR – 7 by charitable/religious trusts:

- Aggregate annual receipts of the projects/institutions run by the trust.

- However, the table asking details about the name and annual receipts of institutes covered under Sections 10(23C)(iiiab), (iiiac), (iiiad) and (iiiae) has been removed.

- Date of registration or approval granted to the trust

- Amount utilized during the year for the stated objects out of surplus sum accumulated during an earlier year.

- There could be a situation when the trust modifies the objects which

do not conform to the conditions of registration. In that case, the

trust is required to take a fresh registration. In this regard the ITR-7

requires:

- Date of change of objects

- Whether application for fresh registration has been made within stipulated time period?

- Whether fresh registration has been granted?

- Date of such fresh registration.

- As per the Finance act, 2017, any donation by a charitable institution to another charitable institution shall not be treated as application of funds. To give effect, the trust shall be required to report the amounts separately to add back into the taxable income.

17. Details of foreign bank account of non-residents

(Relevant for ITR 2, 3, 4, 5, 6 and 7)

The new ITR forms allow non-residents to

furnish details of any one foreign Bank Account for the purpose of

payment of income-tax refund. This would ease the process to transfer

the income tax refund directly the foreign accounts of the

non-residents.

18. Reporting of foreign current payments/receipts:

(Relevant for ITR 6)

The following reporting is mandatory for

assessees who is not liable to get accounts audited under section 44AB

of Income tax act, 1961.

19. CSR Expenditure reporting

(Relevant for ITR 6)

It is compulsory for companies to incur the expenditure as CSR expense under companies act, 2013.

Now a new column has been inserted in ITR 6

for reporting the Corporate Social Responsibility (CSR) expenditures

into the income tax return though these expenses are not allowable under

section 37(1).

The information is based on the ITR forms notified by the CBDT for Assessment year 2018-19.

Article is Authored by CA Neeraj

Kumar and CA Deepak Arya of RAPG & Co., Chartered Accountants and

they can be reached at info@rapg.in

No comments:

Post a Comment