10 Changes in Income Tax for Assessment Year 18-19

sumanth.nca@gmail.com taxguru.in/income-tax/10-changes-in-income-tax-for-assessment-year-18-19.html

taxguru.in/income-tax/10-changes-in-income-tax-for-assessment-year-18-19.html1. Change in Income Tax Slab Rate for AY 2018-19 for Individuals :

The only change in Income Tax Slab Rate is change in the tax rate for income falling between 2,50,000 – 5,00,000, it has reduced from 10%(in AY 17-18) to 5%.

Individual (Resident or Non-Resident), whose age is less than 60 years on the last day of the Relevant Previous Year:

| Taxable income | Tax Rate |

| Up to Rs. 2,50,000 | Nil |

| Rs. 2,50,001 to Rs. 5,00,000 | 5% |

| Rs. 5,00,001 to Rs. 10,00,000 | 20% |

| Above Rs. 10,00,000 | 30% |

Individual (Resident Senior Citizen), Whose age is 60 years or more on the last day of Relevant Previous Year :

| Taxable income | Tax Rate |

| Up to Rs. 3,00,000 | Nil |

| Rs. 3,00,001 to 5,00,000 | 5% |

| Rs. 5,00,001 to 10,00,000 | 20% |

| Above Rs. 10,00,000 | 30% |

Individual (Resident Super Senior Citizen), Whose age is 80 years or more on the last day of Relevant Previous Year :

| Taxable income | Tax Rate |

| Up to Rs. 5,00,000 | Nil |

| Rs. 5,00,001 to 10,00,000 | 20% |

| Above Rs. 10,00,000 | 30% |

Surcharge :

10% of tax where total income exceeds Rs. 50 lakhs

15% of tax where total income exceeds Rs. 1 crore.

Clarity with respect to Applicable rate of Cess :

| Assessment Year (AY) | Rate |

| 18-19 | 3% |

| 19-20 | 4% |

2. Rebate u/s. 87A:

Comparison of Rebate between AY 17-18 and AY 18-19

| AY 17-18 | Particulrs | AY 18-19 |

|

5,000 (or)

100% of Income Tax (Whichever is Lower)

|

Amount of Rebate Allowed

|

2,500 (or)

100% of Income Tax (Whichever is Lower)

|

| Resident Individual Whose Total Income does not exceed 5,00,000 |

Who are eligible for rebate

|

Resident Individual Whose Total Income does not exceed 3,50,000 |

3. APPLICABILITY OF SECTION 234F FEE FOR DEFAULT IN FURNISHING OF INCOME TAX RETURN WITHIN DUE DATES SPECIFIED U/S. 139(1)

| Total Income | Period of Return Actually Filed | Fee (in Rs.) |

| Not Exceeds 5,00,000 | On or Before 31st July,2018 | Nil |

| 1st August,2018 to 31st March,2019 | 1,000 | |

| Exceeds 5,00,000 | On or Before 31st July,2018 | Nil |

| 1st August,2018 to 31st December,2018 | 5,000 | |

| 1st January,2019 to 31st March,2019 | 10,000 |

4. Change of Base Year for Indexation:

Earlier 1st April, 1981 is considered as a

base year for calculating Indexed Cost of Acquisition for the purpose of

Long Term Capital Gain. Now, the same has been changed to 1st April

2001.

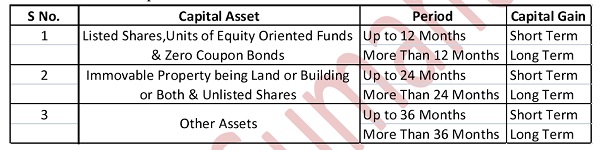

5. Change in the Holding Period of Capital Asset for the purpose of Computation of Capital Gains :

Classification of Capital Asset :

6. Tax Cases can be reopened for up to 10 Years :

The Income Tax Department can now scrutinize

income tax returns up to Previous 10 Years if it suspects undisclosed

income or assets of more than Rs. 50 lakhs. Currently this limit was 6

years.

7. Disallowance of certain deductions if return is not furnished within the Due Date specified u/s. 139(1) :

Earlier, Deductions under sections 80-IA or

80-IAB or 80-IB or 80-IC are not allowed unless he furnishes a return of

his income for such assessment year on or before the due date specified

under section 139(1).

However, this disallowance extended to all similar deductions which are covered under “Heading C”- Deductions in respect of certain incomes in Chapter VIA.

8. :

| Person | Due Date |

| Companies | 30th September |

| persons other than companies, Whose Books of Accounts are not subject to tax audit u/s. 44AB | 31st July |

| persons other than companies, Whose Books of Accounts are subject to Tax Audit u/s. 44AB | 30th September |

| Working Partner of a Firm Whose Books of Accounts are subject to Tax Audit u/s. 44AB | 30th September |

Note : As per Income Tax Act, Person includes

Individuals, HUF, Partnership Firms, Companies, Body of Individuals or

Association of Persons, Local Bodies and Artificial Jurisdictional

Person.

9. Extension of Aadhaar-PAN linking :

CBDT extended the last date for Aadhaar-PAN linking till June 30,2018. If one fails to do so, he/she may not be able to get his/her tax returns processed by tax department.

As per Section 139AA(2) of the Income Tax Act,

Every Person who is having PAN as on July 1, 2017, and eligible to

obtain Aadhaar, must intimate his Aadhaar number to the tax authorities.

10. :

1. Detailed inputs with respect to Income From Salary and House Property :

With respect to Income from Salary, ITR is

made available in such a way we need to enter all the details which are

there in Form 16.

With respect to Income from House Property, We

need to give inputs of Gross Rent received, Taxes paid to Local

Authorities, Interest on Borrowing Capital.

2. Cash deposits during the period of Demonetization fields are removed.

.3. only “Resident and Ordinary Resident” is allowed to file ITR 1.

4. GST No. to be Quoted :

The Assesses filing ITR 3 & ITR 4 would

have to enter GST Registration no. and its Turnover. This is to

Correlate the Direct and Indirect taxes to put a check on tax evasions.

No comments:

Post a Comment