- Aug

- 27

- 2015

Brief- The

article covers Introduction, Residential Status, Tax Rates, Head-wise Taxation

& Deduction available under the Act. Hope you will find it useful in this

Return Filing Season.

Introduction

Charge

of Income Tax

- Income tax is charged in assessment year at rates specified by the Finance Act applicable on 1st April of the relevant assessment year.

- It is charged on the total income of every person for the previous year.

- Gross Total Income (G.T.I):- The aggregate income under the 5 heads of income (viz. Salary, House Property, Business or Profession, Capital Gains & Other Sources) is termed as “Gross Total Income”.

- Total Income (T.I):- Total Income of assessee is gross total income as reduced by the amount permissible as deduction under sections 80C to 80U. Also called “Taxable Income”

Types

of Residential Status

The different types of residential

status are:-

- Resident(R)

- Not Ordinarily Resident (NOR)

- Non-Resident (NR)

RATES OF INCOME TAX (Assessment Year

2015-16)

- In case of every Individual (Men/Women) below the Age of 60 Years.

|

S.No

|

INCOME

|

TAX RATE

|

|

1

|

Up to 250000

|

NIL

|

|

2

|

250000-500000

|

10%

|

|

3

|

500000-1000000

|

20%

|

|

4

|

Above 1000000

|

30%

|

2. In case of resident senior

citizen i.e. age above 60 years but below 80 years

|

S.No

|

INCOME

|

TAX RATE

|

|

1

|

Up to 300000

|

NIL

|

|

2

|

300000-500000

|

10%

|

|

3

|

500000-1000000

|

20%

|

|

4

|

Above 1000000

|

30%

|

Note:

In case of residents individual if their total income is not more than

Rs.500,000 than U/s 87A there is Tax Credit Relief of 10% of Taxable

Income or upto maximum of Rs.2000.

Income

From Salary

Meaning

Salary

includes [section17 (1)] :-

- Wages

- Any annuity on pension

- Any gratuity

- Any fees, commission, bonus, perquisite on profits in lieu of or in addition to any salary on wages

- Any advance of salary

- Any earned leave

- Employers contribution (taxable) towards recognized provident fund.

BASIS

OF CHARGE

Income

is taxable under head “Salaries”, only if there exists Employer – Employee

Relationship between the payer and the payee. The following incomes shall

be chargeable to income-tax under the head “Salaries”:-

- Salary Due

- Advance Salary [u/s 17(1)(v)]

- Arrears of Salary

Note:

- Salary is chargeable on due basis or receipt basis, whichever is earlier.

- Advance salary and Arrears of salary are chargeable to tax on receipt basis only.

Allowances

Allowance

is generally defined as a fixed quantity of money or other substance given

regularly in addition to salary for the purpose of meeting some particular

requirement connected with the services rendered by the employee or as

compensation for unusual conditions of that service.

- Dearness Allowance – It is always Taxable.

- City Compensatory Allowance – It is always Taxable.

- House Rent Allowance

Exemption

In Respect Of House Rent allowance is regulated by rule 2A. The least of the

three given below is Exempt from Tax.

|

1

|

An Amount Equal to 50 % of Salary.

Where Residential House in situated at Bombay, Calcutta, Delhi or Madras and

An Amount Equal to 40 % of Salary where Residential House is situated at any

Other Place.

|

|

2

|

House Rent Allowance Received by

The Employee in Respect of The Period during which Rental Accommodation is

Occupied by the Employee during the Previous Year.

|

|

3

|

The Excess of Rent Paid over 10 %

of Salary.

|

4. Special allowances prescribed as

exempt under section 10(14)

– In the cases given below the amount of exemption under section 10(14) is :–

i. The amount of the allowance ; or

ii. The amount utilized for the

specific purpose for which allowance is given.

Whichever

is lower.

For

e.g.

- Travelling Allowance

- Conveyance Allowance

- Daily Allowance

5. When exemption does not depend

upon expenditure –

- the amount of allowance ; or

- the amount specified in rule 2BB,

Whichever is lower.

Others:

|

Name of allowance

|

Exemption as specified in rule 2BB

|

|

Children education allowance

|

The amount exempt is limited to

Rs. 100 per month per child up to a maximum of two children.

|

|

Hostel expenditure allowance

|

It is exempt from tax to the

extent of Rs. 300 per month per child up to a maximum of two children.

|

|

Transport allowance

|

It is exempt up to Rs. 800 per

month (Rs. 1,600 per month in the case of an employee who is blind or

orthopedically handicapped)

|

TERMINAL

BENEFITS

1. Gratuity [Sec.10(10)] – Gratuity is a retirement benefit. It is generally payable

at the time of cessation of employment and on the basis of duration of service.

Tax treatment of gratuity is given below:

2. PENSION [SEC. 17(1)(ii)] – Pension is chargeable to tax as follows :-

3. Annuity [Sec. 17(1)(ii)] – An annuity payable by a present employer is taxable as

salary even if it is paid voluntarily without any contractual obligation of the

employer. An annuity received from an ex-employer is taxed as profit in lieu of

salary.

3. Annuity [Sec. 17(1)(ii)] – An annuity payable by a present employer is taxable as

salary even if it is paid voluntarily without any contractual obligation of the

employer. An annuity received from an ex-employer is taxed as profit in lieu of

salary.

4. Retrenchment compensation [Sec.

10(10B)] – Compensation received by a

workman at the time of retrenchment is exempt from tax to the extent of the

lower of the following:

a. an amount calculated in

accordance with the provisions of sec. 25F(b) of the Industrial Disputes Act,

1947; or

b. such amount as notified by the

Government (i.e., Rs, 5, 00, 000); or

c. the amount received.

5. Compensation received at the time

of Voluntary Retirement [sec.10 (10C)]

– Compensation received at the time of voluntary retirement is exempt from tax,

subject to certain conditions. Maximum amount of exemption is Rs. 500000.

Provident

Fund

Provident

Fund Scheme is a welfare scheme for the benefit of employees. The employee

contributes certain sum to this fund every month and the employer also

contributes certain sum to the provident fund in employees A/c. the employers

contribution to the extent of 12% is not chargeable to tax.

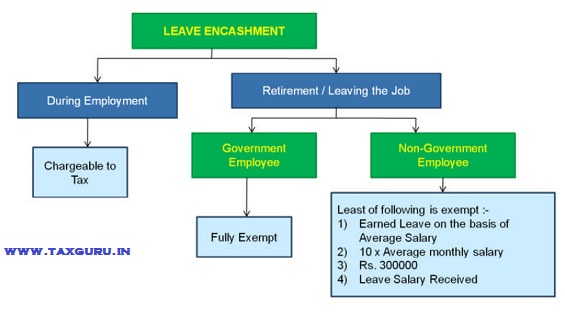

LEAVE

SALARY

Encashment

of leave by surrendering leave standing to one’s credit is known as “leave

salary”.

Deductions Admissible in Computing Income under head

‘SALARIES’

Deductions Admissible in Computing Income under head

‘SALARIES’

1. Employment Tax / Professional Tax

[Sec.16(iii)]: Any sum paid by assessee on

account of a tax on employment within the meaning of Article 276(2). Under the

said article employment tax cannot exceed Rs. 2500 p.a.

Relief

in respect of Advance or Arrears of Salary u/s 89

When

an assessee is in receipt of a sum in the nature of salary, being paid in

arrears or in advance, due to which his total income is assessed at a rate

higher than that at which it would otherwise have been assessed, Relief is

granted on an application made by the assessee to the assessing officer.

Income

From House Property

Basis

of Charge

- The basis of charge of income under the head ‘income from house property’ is the Annual Value of the property.

- Income from house property is charged to tax on Notional Basis, as generally tax is not on receipt of income but on the inherent potential of the house property to generate income.

Conditions

to be Satisfied

1. The property must consist of

buildings or lands appurtenant to such buildings.

2. The assessee must be the owner

of such house property.

3. The property should not be used

by the owner thereof for the purpose of any business or profession carried on

by him, the profits of which are chargeable to tax.

- In case of Self-occupied House Property Net Annual Value is always Zero.

- Since NAV is zero, the municipal taxes paid by the owner of the house are not deductible.

Deduction

Admissible u/s 24

i. Statutory deduction :- 30% of Annual Value (i.e.30% of NAV)

ii. Interest payable on capital

borrowed for acquisition, construction, repair, renewal or reconstruction of

house property :- Actual amount of interest for

the year on accrual basis plus 1/5th of the interest,

if any, pertaining to the pre-acquisition or pre-construction period.

Deduction

for Interest on Capital Borrowed in case of SOP

Maximum

limit of deduction in respect of interest on capital borrowed in case of a

Self-occupied property whose annual value is assessed at NIL, is Rs. 1,50,000

|

CASE

|

MAXIMUM DEDUCTION

|

|

Interest on capital borrowed on or

after 1-4-1999 for acquisition or construction of house

|

1,50,000

|

|

In any other case

|

30,000

|

Income

From Other Sources

General

[Section 56(1)]

Income

of every kind, which is not to be excluded from the total income and not

chargeable to tax under any other head, shall be chargeable under the head

“Income from Other Sources”.

Specific

Income [Section 56(2)]

- Dividends.

- Lottery winnings etc

- Income by way of interest on securities if not chargeable as Profits and Gains of Business or Profession

- Interest on bank deposits and loans

- Cash Gifts exceeding Rs. 50,000,

Cash

Gifts

Except,

- From Relatives

- On the Marriage Occasion

- By will or heritance

- In contemplation of death of payer

- From local authority

- From Charitable Trust regtd u/s12AA

- From trust, Foundation etc u/s 10(23c)

Deductions

Under Chapter VI-A

Introduction

- Deductions to be made [Section 80A] :

The

total income of an assessee is to be computed after making deductions

permissible u/s 80C to 80U. However, the aggregate amount of deductions cannot

exceed the Gross Total Income.

- No deduction from certain (following) Incomes :

- Long term Capital Gains referred u/s 112, and Short Term Capital gains referred u/s 111A.

- Winnings from lotteries, races, etc. as referred to in section 115BB.

Deduction

for Payment of Life Insurance Premia, etc., [Section 80C]

Deduction

under this section is allowed as follows –

- Deduction is available only in respect of ‘specified sums’ actually paid or deposited during the previous year (sum not actually paid and outstanding is not allowed)

- Specified sums must have been paid/deposited by an Individual or HUF; and

- The total amount of deduction under this section is subject to a maximum limit of Rs.1,50,000

Investment

Options under Section 80C

- PPF

- NSC’s

- LIP Payment

- Children’s Tuition Fee Payment

- Principal Repayments on Loan for purchase of house property

- ULIPS, ELSS; etc.

- 5-year Deposit of Post Office

- Notified Pension fund, Bonds of NABARD, Deposit Scheme, Mutual Fund or UTI .,etc;

Contribution

to Certain Pension Funds [Section 80CCC]

–

Amount paid or deposited by individual in the previous year –

- out of his income chargeable to tax

- to effect or keep in force a contract for any annuity plan of LIC or any other insurer

- for receiving pension from the fund referred to in section 10(23AAB).

–

Quantum of Deduction: Deduction shall be allowed to the extent of lower

of the following –

- Amount so paid or deposited; or

- 1,00,000

Contribution

to Pension Account [Sec. 80CCD]

Deduction

to the Extent: –

|

Maximum 10% of Salary (In case of

employment)

|

|

Maximum 10% of Gross Total Income

(In case of Self-employment)

|

|

Rs.100,000/-

|

Aggregate

Limit u/s 80C, 80CCC & 80CCD

The

aggregate amount of deductions under section 80C, section 80CCC and section

80CCD shall not, in any case, exceed Rs.1,50,000.

Deduction

In Respect Of Health Insurance Premia [Sec. 80D]

- Deduction is available upto Rs. 20,000/- for Senior Citizens

- 15,000 in other cases for insurance of self, spouse and dependent children.

- Additionally 20,000/- if parents are senior citizens and 15,000/- in other cases

- So Total limit summing to Rs.40,000/- and within it Rs.5,000 limit of preventive health Check-up

Maintenance

of A Dependant Being Person With Disability [Section 80DD]

Deduction

is available in respect of –

- expenditure incurred for medical / treatment / nursing / training/ rehabilitation, or

- Amount paid under scheme LIC / UTI other insurer approved by CBDT for maintenance, of a “dependant”, being a person with disability.

Deduction

shall be allowed to the extent of –

- 50,000 (Rs. 1,00,000 in case of dependant suffering with severe disability), irrespective of expenditure incurred or sum paid.

Medical

Expenditure on self or Dependent Relative, etc. [Sec. 80DDB]

Deduction

is available in respect of sum actually paid during previous year for medical

treatment of prescribed disease or ailment for the following –

- In case of individual: himself or his spouse, children, parents, brothers and sisters,

- In case of HUF: its member(s),

- Dependant mainly on such individual or HUF for his support and maintenance.

Deduction

shall be available to the extent of lower of the following –

- sum actually paid; or

- 40,000 (Rs. 60,000 in case of a senior citizen).

Deduction

in respect of Interest on Loan taken for Higher Education [Sec.80E]

- Deduction is available in respect of sum paid by way of interest on loan taken –

- for his higher education, or

- for the higher education of his relative.

- 100% of the amount of interest on such loan Deduction will be admissible.

Deduction

in respect of Donations [Section 80G]

- Deductions are eligible for deduction upto either 100% or 50% with or without restriction.

- There is specified list for each of the four categories.

- If donation is given in the form of cash for amount over Rs. 10,000 then deduction is not available.

Deductions

in respect of House Rent [Sec.80GG]

- Rent actually paid for any furnished or unfurnished residential accommodation occupied by the Individual, who is not in receipt of any House Rent Allowance (HRA).

- Should not have Self-Occupied property.

- The deduction shall be allowed to the extent of least of the following –

- 2,000 per month;

- 25% of adjusted total income;

- Rent paid less 10% of adjusted Total Income.

Deduction

on Savings Bank Account [Sec.80TTA]

- Deduction of Rs. 10,000 in respect of Interest on deposits in Savings account is available.

- No time deposits or fixed deposits are eligible for deduction

- Savings account can be with a Bank, co-operative society or post office.

Deduction

in respect of person with Disability [Section 80U]

- Individual who suffers from a physical disability (including blindness) or mental retardation is eligible for deductions of Rs.50,000

- In case of severe disability, Rs.100,000 is allowable.

- Certificate from Govt. Doctor is necessary.

- See more at:

http://taxguru.in/income-tax/income-tax-provisions-individual-salaried-ay-201516.html#sthash.Tu1O1peP.dpuf